Digitisation Strategies: A Comparative Analysis of Banking and Insurance

Introduction

In today's rapidly evolving financial landscape, both the banking and insurance sectors are undergoing significant transformations driven by digitisation. These industries, though distinct in their core functions, share common goals of enhancing customer experience, improving operational efficiency, and staying competitive in the digital age. This blog post provides a comparative analysis of the digitisation strategies adopted by banks and insurance companies.

The Drive for Digitisation in Banking

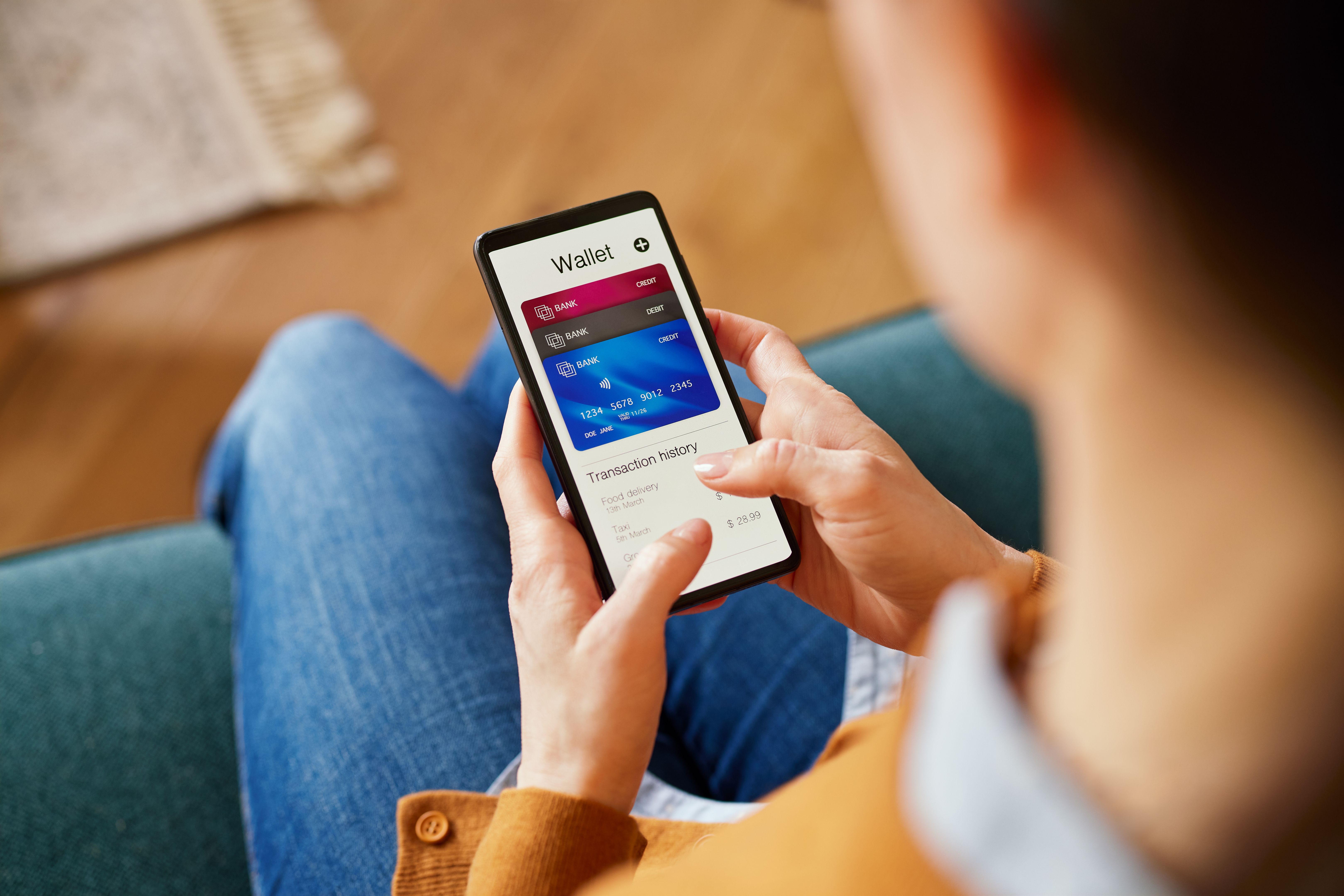

Banks have been at the forefront of digitisation, primarily due to the increasing demand for online and mobile banking services. The need to provide seamless, anytime-anywhere access to banking services has pushed banks to invest heavily in digital technologies.

One of the main strategies involves the implementation of robust mobile banking applications. These apps offer customers the convenience of handling transactions, checking balances, and even applying for loans right from their smartphones. Furthermore, banks are leveraging artificial intelligence (AI) and machine learning (ML) to offer personalized financial advice and detect fraudulent activities.

Embracing Technology in Insurance

The insurance industry, traditionally known for its reliance on paper-based processes, is also embracing digitisation. Insurers are adopting technology to streamline operations, enhance customer interactions, and improve risk management.

Insurtech solutions are revolutionizing how policies are underwritten and claims are processed. By utilizing AI, insurers can assess risks more accurately and tailor policies to individual needs. Additionally, the implementation of chatbots in customer service is helping insurers provide real-time assistance and improve customer satisfaction.

Comparative Analysis: Banking vs. Insurance

Despite sharing the goal of digitisation, banks and insurance companies face unique challenges and opportunities in their digital transformations.

Customer Interaction

Banks can offer instant transactions and real-time account management through digital channels. In contrast, insurance companies focus more on providing comprehensive policy information and simplifying claims processes online.

Risk Management

Banks rely on digital tools to monitor transactions and prevent fraud. They use advanced algorithms to detect unusual patterns and secure customer data. Insurance companies, however, use predictive analytics to improve underwriting accuracy and fraud detection capabilities.

Future Prospects

Looking ahead, both industries are expected to deepen their digital engagements. Banks will likely continue enhancing their digital ecosystems by integrating fintech partnerships and expanding the use of blockchain technology for secure transactions.

Insurance companies will further explore IoT devices and telematics to collect real-time data for dynamic pricing models. This data-driven approach will enable more personalized insurance solutions that reflect actual usage and behavior.

Conclusion

The digitisation strategies of banks and insurance companies highlight their commitment to evolving with technological advancements. While each industry has its unique path, the ultimate aim remains consistent—delivering superior service and strengthening customer loyalty in a digital-first world.